When Should I Contribute to My RRSP?

(Five-minute read time)

Knowing when to contribute to your RRSP depends on your income now and in the future. Since RRSP contributions lower your taxable income for the year you contribute but are taxed when withdrawn, timing is key.

In this article, we’ll break down how RRSPs work and when it makes the most sense to contribute to yours.

Want to Learn More About Investing?

Check out our additional articles:

How to Effectively Use Your TFSA and RRSP

RRSPs vs. TFSAs: The Basics

A Registered Retirement Savings Plan (RRSP) is a savings account registered with the Canadian federal government, designed to help Canadians save for a comfortable retirement. There’s no minimum age to open an RRSP account in Canada.

Funds contributed to an RRSP are exempt from being taxed in the year of the contribution, and any investment income earned from investments within the RRSP can grow tax-deferred inside the RRSP. Any money within an RRSP is taxed at the time of withdrawal.

A Tax-Free Savings Account is a general-purpose savings account that allows the account holder to make contributions each year and withdraw funds at any given time. Every Canadian resident 18 years of age or older and with a valid SIN can open a TFSA.

TFSAs are registered, tax-advantaged accounts. While contributions to a TFSA are not tax-deductible, the value inside the TFSA grows tax-free, and the account owner can withdraw funds at any time and avoid paying taxes on those withdrawals.

“Think about your tax rate. If your tax rate at the time of contribution is higher than your tax rate will be at the time of withdrawal, an RRSP is likely the superior choice and will deliver a higher net rate of return. If your current tax rate is lower than when you plan to withdraw funds, a TFSA will provide a higher return.”

Maximize RRSP benefits by contributing at the right time.

Book a call with us to find out how you can optimize tax benefits and enhance your retirement savings.

How Much Can I Contribute to My RRSP This Year?

Contribution limits for RRSP accounts are based on the income of the account owner. Generally, the RRSP contribution room is 18% of the earned income reported on the tax return of the previous year, up to a specified maximum. That maximum is a CRA-determined maximum contribution where, even if 18% of your income from the previous year exceeds that number, you may only contribute the CRA-determined maximum.

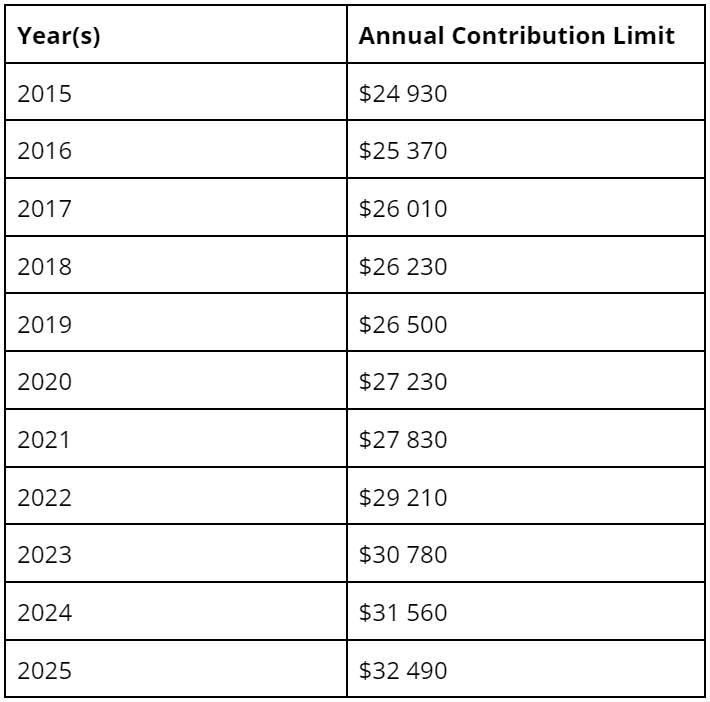

Here are the maximum yearly RRSP contribution limits from 2015 to 2025:

Pension adjustments can also affect a person’s RRSP contribution room.

For RRSPs, any unused contribution room is carried forward and added to the next year’s contribution limit. Any money earned through investments in either account type does not affect the contribution limit.

Overcontributing to your RRSP comes with penalties, so be sure to keep track of your contribution room and the amounts contributed in order to avoid incurring penalties. Your financial advisor will be able to help guide you in this and ensure that all RRSP activity is within the limits established by the CRA.

Does My Income Matter for Timing RRSP My Contributions?

Your income will likely change over time, which can impact when it's best to contribute to an RRSP. In Canada, people in their 20s and 30s typically earn lower incomes, with the average income around $55,000 for those aged 25-34. By the time they reach their 40s and early 50s, incomes usually peak, averaging around $72,800 to $77,400. After age 65, earnings often decrease, earning an average of $48,600 or less (Source: Statistics Canada, 2022). Since RRSP contributions reduce your taxable income, the best time to contribute is when you're earning more so you can get the biggest tax deduction. If you're in a lower income bracket, a TFSA might be a better option until your income increases.

Try this RRSP Contribution Strategy Based on Your Career Stage:

Early Career: At this stage, individuals generally have lower incomes. Contributing to a Tax-Free Savings Account (TFSA) might be more advantageous, as withdrawals are tax-free and contribution room is regained in the following year.

Mid-Career: As income rises, transitioning to RRSP contributions can be beneficial. The tax deductions can offset higher taxable income, and investments grow tax-deferred until retirement.

Approaching Retirement: If your income decreases, TFSA contributions may become more advantageous, but it's essential to consider your current tax bracket and future income needs.

Key Considerations for RRSP

Contribution Limits: You can contribute up to 18% of your earned income from the previous year, with a maximum limit of $32,490 for 2025. If you don’t use your full contribution room, it carries forward to future years.

Over-Contribution Penalties: The government allows a $2,000 buffer for RRSP over-contributions without penalties. If you go over that, you’ll face a 1% penalty per month on the extra amount until it’s removed.

Tax on Early Withdrawals: If you take money out of your RRSP before retirement, it gets added to your income for that year, meaning you’ll pay tax on it at your current rate. This could push you into a higher tax bracket, resulting in an even bigger tax hit.

-

Funds contributed to an RRSP are tax-deductible at the time of contribution, but they are taxed upon withdrawal (as well as any funds gained through investments within the RRSP).

A person’s RRSP reaches maturity on the last day of the calendar year that person turns 71. At this point, the RRSP funds can be accessed through three maturity options: a lump sum withdrawal, converting to a Registered Retirement Income Fund (RRIF), or purchasing an annuity.

Should you decide to withdraw from an RRSP before reaching maturity, here are the implications to be aware of:

You must pay a withholding tax. This amount varies depending on the amount withdrawn and the account owner’s province of residence.

You must pay income tax. Withdrawals are reported on your tax return as income.

You impact your tax-deferred compounding. Since RRSP contributions can compound over time, making even a minor withdrawal may impact your savings down the road.

You lose contribution room. Funds withdrawn from an RRSP do not regenerate as contribution room the following year. That contribution room is permanently lost.

Funds may be withdrawn from an RRSP and tax-deferred if the funds are used to either purchase a first home or finance education through the Home Buyers’ Plan (HBP) or Lifelong Learning Plan (LLP) respectively.

RRSP vs. TFSA: When Should I Contribute?

When deciding when and where to allot your funds, there are a few things to consider.

Think about your tax rate. If your tax rate at the time of contribution is higher than your tax rate will be at the time of withdrawal, an RRSP is likely the superior choice and will deliver a higher net rate of return. If your current tax rate is lower than when you plan to withdraw funds, a TFSA will provide a higher return.

In general, RRSPs are most effective when used for retirement savings while TFSAs can be used to save for retirement as well as other, shorter-term purchases.

There are many factors to consider when it comes to determining the best path for your money: your age, current income, projected income, assets, financial goals, life goals, and so on. Staying informed regarding the rules and regulations of the various registered accounts in Canada provides you with a strong foundation that you can use to build a financial strategy and allot your funds wisely.

Aligning your RRSP contributions with your income trajectory can optimize tax benefits and enhance retirement savings. Consulting with a financial advisor can provide personalized guidance tailored to your financial goals and circumstances; book a call with us at WealthTrack today.

Recognized By

Interested in Learning More About Investing?

Check out our additional resources: