What Should I Do with My Tax Refund?

(Four-minute read time)

Receiving a tax refund is a great way to put some pep in your step. Tax refund day is a great day! A tax refund can often feel like a bonus of sorts, providing some extra, unanticipated money that you can put towards anything you’d like.

When we receive funds we weren’t counting on receiving, it’s easy to justify throwing that money towards something spontaneous, or something typically thought of as luxurious. Often, tax refunds are spent recklessly on purchases that wouldn’t normally make the cut in a regular day-to-day budget. And you know what, that’s okay!

Splurging from time to time isn’t a horrible thing, and in fact, there are some real benefits to letting loose once in a while (as long as you don’t go overboard or compromise your overarching financial goals). But what if you don’t want to do that with this year’s tax return? What if you want to be more intentional and prioritize growing your wealth rather than short-lived bursts of luxury?

We’ve got you covered. Here are five forward-thinking ways to use your tax return that will contribute to your long-term financial well-being and set you on a path to future prosperity!

1. Contribute to an Emergency Fund

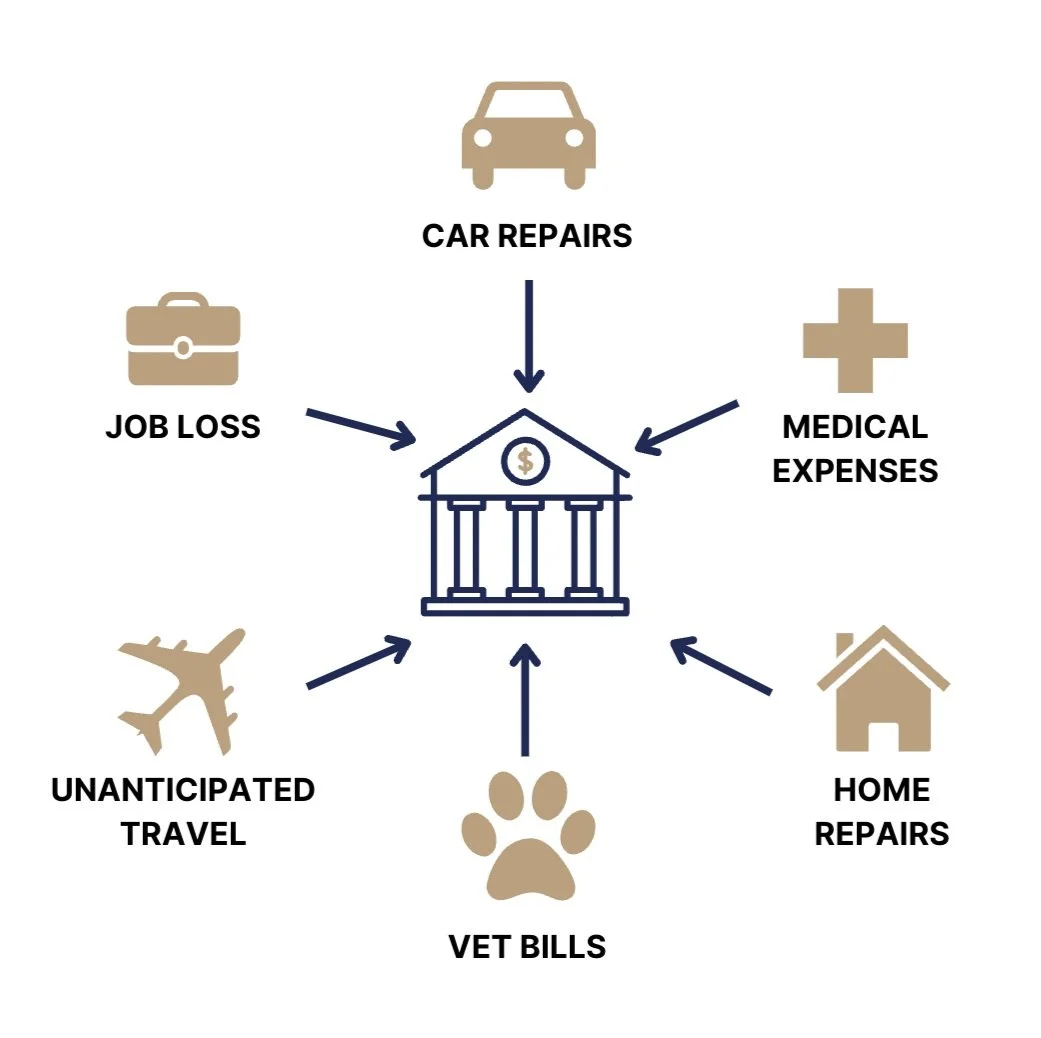

An emergency is a crucial element of any personal finance plan. Best kept in a high-interest savings account, this is a sum of money set aside to only be used in case of emergency. Whether that’s a healthcare crisis, a sudden auto or home repair, or anything else that involves an unexpected but necessary immediate payment, an emergency fund exists to provide you with the cash you need at a moment’s notice without needing to sell off investments or engage in risky loans.

It’s generally advised to keep three to six months’ worth of expenses in an emergency fund, or more if you have dependents. Should you lose your job, this fund will keep you afloat until you’re back on your feet. If you don’t have three to six months’ worth of expenses stashed away just yet, don’t worry – begin with a goal of saving for the cost of one month, and continue to grow the fund as time goes on.

If your emergency fund isn’t quite where you’d like it to be, it’s the perfect allocation for this year’s tax return.

To learn more about budgeting, read our article: How to Make a Budget

2. Contribute to a Sinking Fund

Similar to an emergency, a sinking fund should be kept in a high-interest savings account so that it’s accessible when you need it. However, sinking funds are used to slowly save toward anticipated purchases.

This might include things like a new laptop or phone, a new car, a vacation, or purchasing holiday gifts. Any significant purchase that you can expect and plan for is a perfect situation to establish a dedicated sinking fund.

By utilizing sinking funds, you can intentionally save and factor those more significant purchases into your budget over a period of time. It’s also easy to keep track of how you’re progressing toward your saving goals, as the money you dedicate to a particular purchase is kept separate from your emergency fund or other savings.

So, if you have extra money lying around from your tax return this year, you might want to consider putting it toward establishing or filling out a sinking fund!

3. Put It Toward Debt

Debt of any kind (and especially high-interest debt) is a burden nobody likes to have. Putting your tax return dollars towards paying off more than the minimum required payment, or even paying off debt completely, can help you achieve financial freedom while also drastically reducing the stresses associated with carrying debt.

Doing so can help to free up your cash flow, and if you’re able to use your tax return to pay off a debt completely, you can then allocate your funds towards different areas moving forward. If you’ve got debt looming over your head and the burden of constant payments, this might be a great opportunity to put your tax return to good use this year.

4. Pay Down Your Mortgage

As your biggest expense, the interest on your mortgage can be hundreds or thousands of dollars each month. Paying down your mortgage will reduce your interest cost for years to come. Something to note is that most mortgages will allow you to make an annual lump-sum payment, which could be a fantastic use for your tax refund dollars.

Regardless of how much you’re able to contribute, every little bit counts when it comes to paying off your mortgage. Push yourself closer to that goal and pay down your mortgage with the money you receive from your tax return!

Learn more: How to Pay Off Your Mortgage Faster in Ontario.

5. Invest

Anytime you find yourself with some extra money lying around and all of your financial bases covered, investing those funds will almost always be the right choice. There are all sorts of options when it comes to investing strategy from risk tolerance to which assets to invest in, but regardless of your particular choices, investment is a powerful vehicle that allows you to put your dollars to work and grow your wealth.

If you’re not entirely sure how to navigate the world of investment, consulting a financial advisor is a great way to make savvy decisions that align with your long-term financial goals, and it can help you to enter investments with confidence.

Investing your tax return money is a fantastic strategy for growing your wealth, and future you will surely thank you.

Looking for more ideas for how to allocate your tax return, or personal advice relevant to your particular financial situation? Look no further than the experts here at WealthTrack. We’re here to guide you on the road to prosperity and help you to reach your financial goals! Contact us today.

Recognized By

Interested in Learning More About Investing?

Check out our additional resources: